Tips for Budgeting Your Next Vehicle Purchase

It’s no secret that cars have become quite expensive, and not just new ones. As new car prices rise, demand for used cars increases, pushing their prices higher. We see this firsthand at Alderman Automotive, where we buy used cars every day. Meanwhile, the question of “How much car can I afford?” is being asked more often these days. While we can’t answer that, we can offer some guidelines to help.

Factors and More Factors

We can’t answer because there are so many factors that can only be estimated. How much you make is an obvious one, but probably more important is how much you spend. Are you paying rent, a mortgage, or a student loan? Are you single? Married? A parent? Is your job salaried? Or does it vary with commissions, hours, or other factors?

Let’s start with this. If you can buy a vehicle outright with cash, do it. There’s no interest to pay, it is a pretty good negotiating tactic, and you only need to worry about ownership and operating costs. However, for most people, especially with new or recent models involved, the options come down to financing or leasing. Since leasing almost always involves a new vehicle, and we are a used-vehicle dealer, we will focus on financing.

Affordability mainly depends on how much you can put down and how much you can afford to pay each month; the larger the down payment, the lower your monthly payments will be for a given loan term. You know how much you have available for the down payment, and you may want to balance when you want to buy with how much more you can save.

A General Budgeting Guideline

Beyond the down payment, affordability may seem to revolve around the monthly payment, but not entirely. Again, everyone’s financial situation can be unique, and their vehicle budget will vary accordingly. However, there is a general rule of thumb: Your total vehicle expenses should be at or below 15% of your net income, which is to say after taxes, Social Security, and so on. Your “take-home pay,” in other words.

Notice that the term was “total vehicle expenses,” so beyond your monthly payment, this would include insurance, fuel costs, and regular maintenance, which can also include minor repairs. (Hopefully, the large ones are covered by the insurance.) Again, this varies for everyone. A young single male will pay more for insurance on the same vehicle than a middle-aged married woman with a good record, simply because statistically, the latter is a better risk for the insurance carrier.

Some General Examples

USAA provided this simple chart based on the 15% rule of thumb.

| Annual pay | Monthly pre-tax | Monthly after tax (estimated) | Total cost of ownership (payment insurance, maintenance, fuel, etc.) |

| $25,000 | $2,083 | $1,728 | $260 a month |

| $50,000 | $4,167 | $3,352 | $503 a month |

| $75,000 | $6,250 | $4,817 | $723 a month |

| $100,000 | $8,333 | $6,265 | $940 a month |

| $125,000 | $10,417 | $7,685 | $1,153 a month |

Examples based on a single filer taking one federal, state, and local allowance with no pre-tax or post-tax deductions. Your specific tax situation can vary widely from these examples. Be sure to consult a tax professional regarding your specific situation.

They then made an example of how this could break down for an individual in the $50,000 bracket:

Monthly Vehicle Expenses

Car payment $303

Auto insurance $90

Maintenance $50

Fuel $60

Total cost of ownership $503

This isn’t to say that if you make $50K, your car payment should be around $300. Instead, you need to create a similar breakdown for your own situation. The tricky part is that everything varies depending on the vehicle you’re considering. Fuel costs depend in part on the vehicle’s expected MPG. Insurance varies by model (based on the vehicle’s cost and type), and maintenance costs will also differ depending on the vehicle’s model, age, and condition.

Even if you can purchase your vehicle with cash, you need to factor everything above, except the car payment.

Don’t Focus Entirely on Payments

Be aware that all this focus on the monthly payment can lead you into a financing trap if you’re not careful. That is because the payment will be lower the longer the loan term, which makes it easier to fit into your monthly budget. But the longer the term, the more you pay overall because the total interest increases with the length of the loan.

Another problem with long loan terms is that you can end up owing more than the vehicle’s worth because of depreciation over time. This can become problematic if you need to sell the vehicle, as your lender not only gets every penny of the sale but possibly thousands more if the vehicle sells for less than the remaining loan balance. This situation is called being upside-down, a term established long before its use in “Stranger Things,” but it’s almost as frightening. A larger down payment or shorter loan terms are the best ways to avoid being upside-down.

Again, we can’t recommend the ideal loan term for you, but you should be cautious of anything longer than four years.

Predicting the Future

The loan term brings up another important consideration. What life changes do you anticipate during the loan period? If you’re single, do you think you might get married? If you’re married, do you expect to have kids? If you have kids, when will they start driving? Can the car you choose eventually be passed down to one of them? Or do you foresee a career change, with a new location and a different commute? Also, if you are disappointed by how little you have for a down payment this time, do you want more on hand the next time? This may all be just speculation, but it’s worth considering.

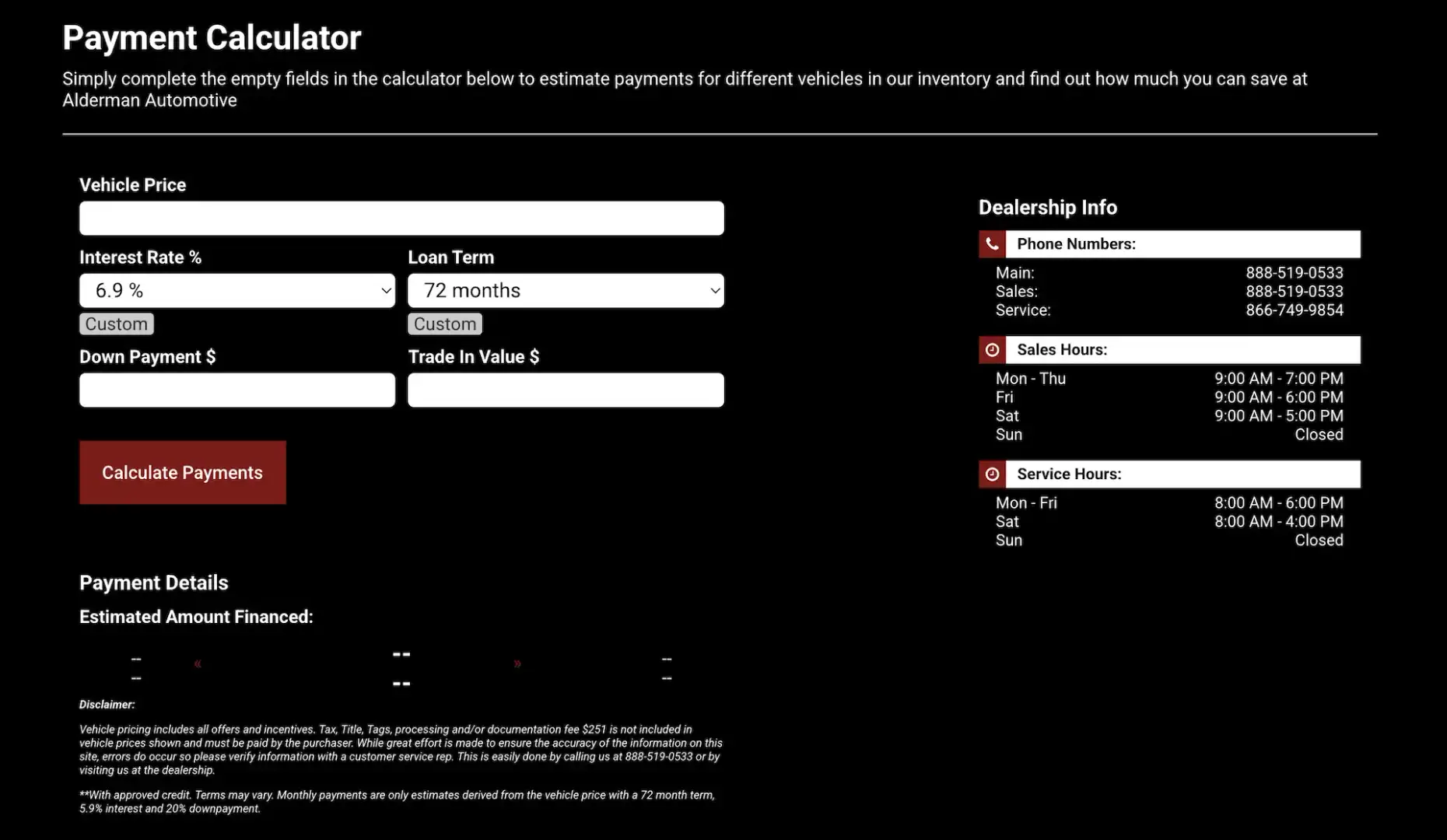

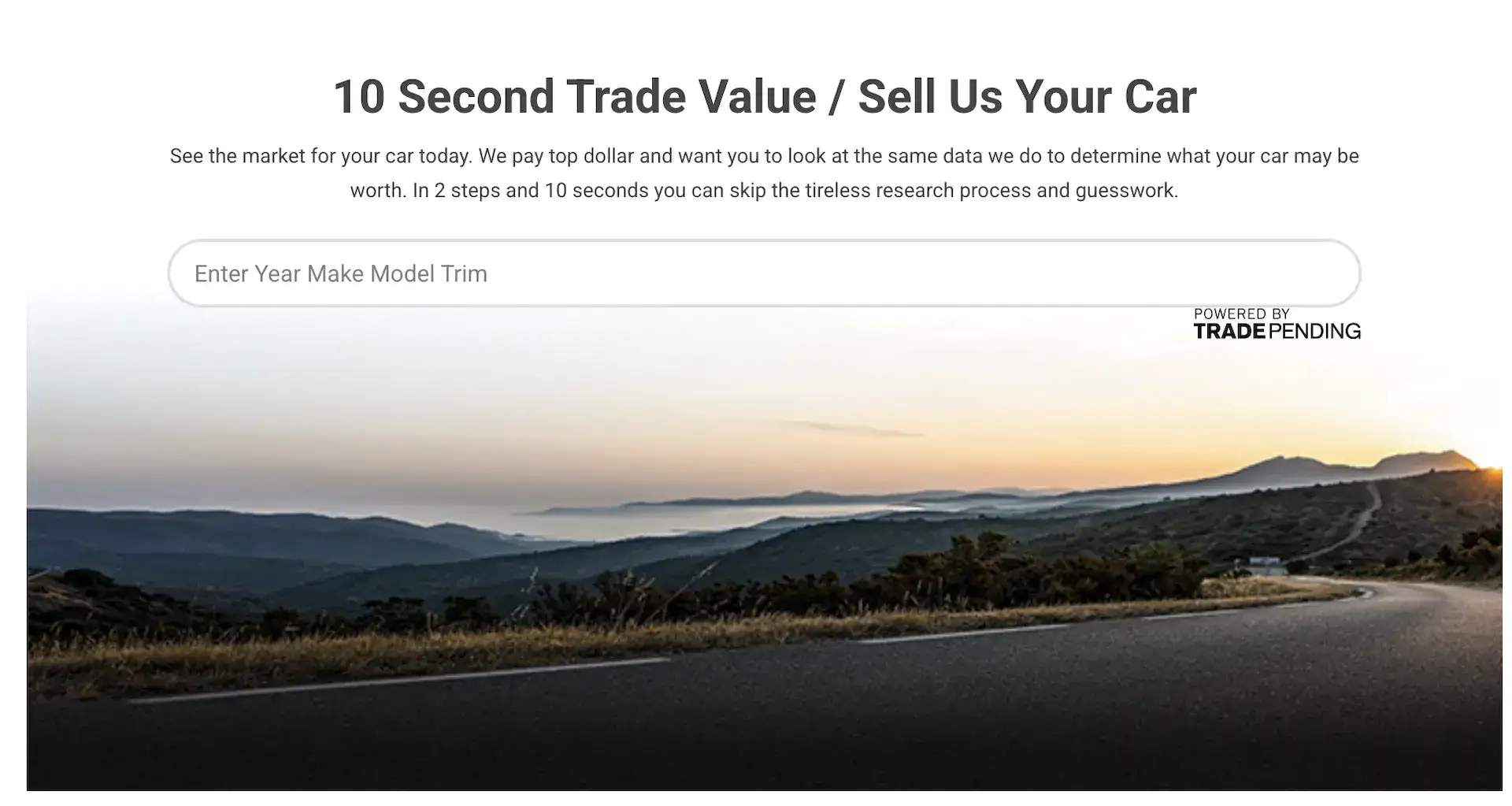

We know that what we’ve provided are more questions than answers, but these are important questions to ask, and only you can answer them. Once you think you have some guidelines to follow, it wouldn’t surprise us if you decide that a used vehicle makes more sense than a new one. If you live in the greater Indianapolis area, take your budget and explore the wide and diverse selection in the Alderman Automotive inventory. We even offer a quick way to view vehicles priced under $25,000, or you can easily set your own price range. Mileage is provided for each model, we have a convenient payment calculator, and even a quick trade-in estimator to help you start the calculations above. In any case, we wish you the best outcome from your careful budgeting.

0 comment(s) so far on Tips for Budgeting Your Next Vehicle Purchase